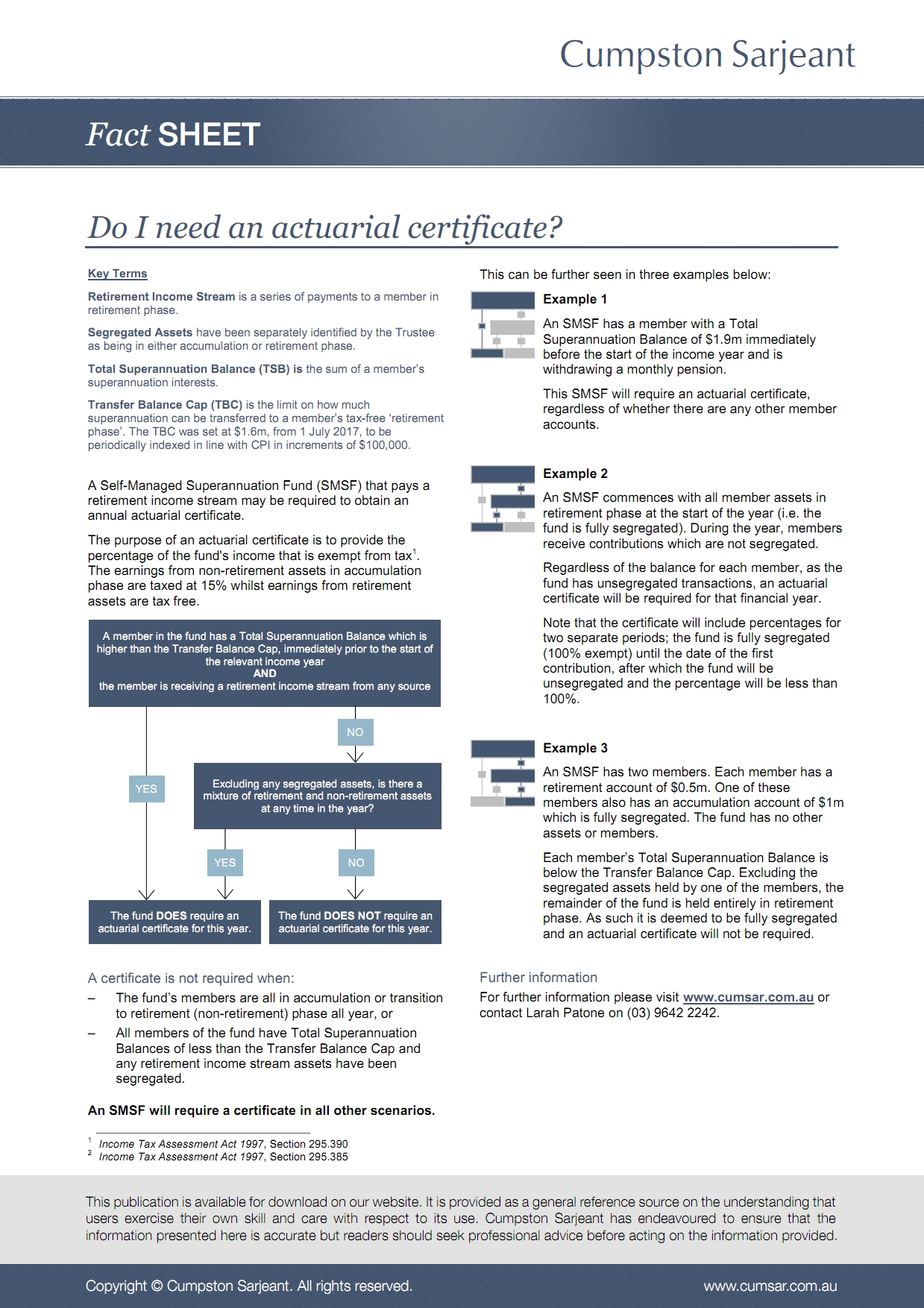

A Self-Managed Superannuation Fund (SMSF) that pays a retirement income stream may be required to obtain an annual actuarial certificate.

The purpose of an actuarial certificate is to provide the percentage of the fund’s income that is exempt from tax.1 The earnings from non-retirement assets in accumulation phase are taxed at 15% whilst earnings from retirement assets are tax free.

A certificate is not required when:

- The fund’s members are all in accumulation or transition to retirement (non-retirement) phase all year, or

- All members of the fund have Total Superannuation Balances of less than the Transfer Balance Cap and any retirement income stream assets have been segregated.

An SMSF will require a certificate in all other scenarios.

Example 1

An SMSF has a member with a Total Superannuation Balance of $1.9m immediately before the start of the income year and is withdrawing a monthly pension.

This SMSF will require an actuarial certificate, regardless of whether there are any other member accounts.

Example 2

An SMSF commences with all member assets in retirement phase at the start of the year (i.e. the fund is fully segregated). During the year, members receive contributions which are not segregated.

Regardless of the balance for each member, as the fund has unsegregated transactions, an actuarial certificate will be required for that financial year.

Note that the certificate will include percentages for two separate periods; the fund is fully segregated (100% exempt) until the date of the first contribution, after which the fund will be unsegregated and the percentage will be less than 100%.

Example 3

An SMSF has two members. Each member has a retirement account of $0.5m. One of these members also has an accumulation account of $1m which is fully segregated. The fund has no other assets or members.

Each member’s Total Superannuation Balance is below the Transfer Balance Cap. Excluding the segregated assets held by one of the members, the remainder of the fund is held entirely in retirement phase. As such it is deemed to be fully segregated and an actuarial certificate will not be required.

Key terms:

- Retirement Income Stream is a series of payments to a member in retirement phase.

- Segregated Assets have been separately identified by the Trustee as being in either accumulation or retirement phase.

- Total Superannuation Balance (TSB) is the sum of a member’s superannuation interests.

- Transfer Balance Cap (TBC) is the limit on how much superannuation can be transferred to a member’s tax-free ‘retirement phase’. The TBC was set at $1.6m, from 1 July 2017, to be periodically indexed in line with CPI in increments of $100,000.

Further information

Larah Patone is one of our actuarial certificate specialists. Contact Larah on (03) 9642 2242.

Download fact sheet

References

1 Income Tax Assessment Act 1997, Section 295.390

2 Income Tax Assessment Act 1997, Section 295.385